Over the next 20 years, health care spending in the U.S. will migrate toward well-being and the early detection of disease, away from the funding of America’s sick-care system, according to Breaking the cost curve, a forecast of U.S. health economics in the year 2040 from Deloitte.

Over the next 20 years, health care spending in the U.S. will migrate toward well-being and the early detection of disease, away from the funding of America’s sick-care system, according to Breaking the cost curve, a forecast of U.S. health economics in the year 2040 from Deloitte.

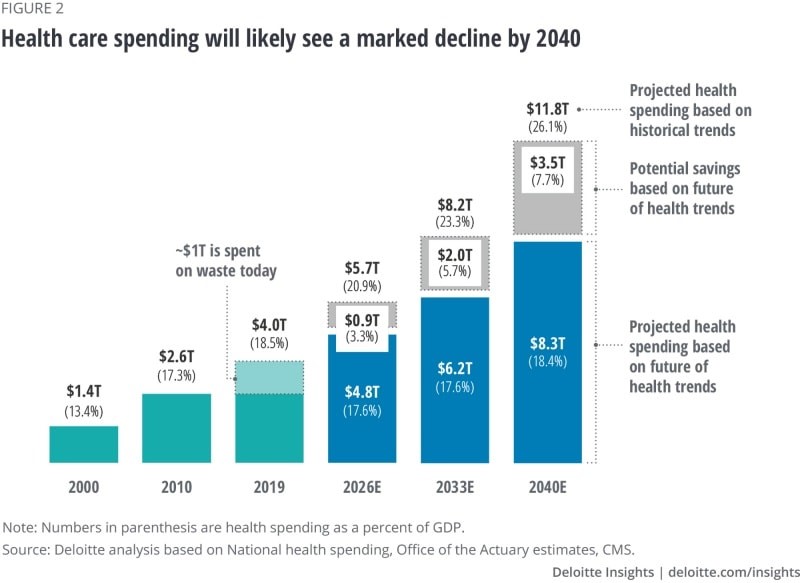

Current spending on health care in America is roughly $4 trillion (with a “t”) dollars, approaching 20% of the nation’s economy.

By 2040, spending is projected to be $8.3 trillion based on future health trends — not historic workflows and delivery mechanisms which would consume an additional $3.5 trillion — close to what we are spending today.

Interestingly that $8.3 trillion spend represents about the same proportion of today’s health care spending, roughly $1 in $5 of national spending.

Deloitte’s analysis is something of a contrarian view given the never-ending upward cost-curve that has been stubborn to bend for decades.

The COVID-19 pandemic has, in fact, had a positive impact on spending per se given the volume-based nature of U.S. health care and that volumes turned downward in 2020.

But letting a virulent public health crisis manage the downturn in American health spending is hardly an optimal hands-on, strategic approach to improving a nation’s health system, let alone a vision to drive health equity, quality improvement and sustainability for patients and care providers.

But letting a virulent public health crisis manage the downturn in American health spending is hardly an optimal hands-on, strategic approach to improving a nation’s health system, let alone a vision to drive health equity, quality improvement and sustainability for patients and care providers.

Deloitte’s actuaries actually developed this analysis using data from before the coronavirus pandemic.

The top-line is that technology innovations, early disease detection and prevention, and consumer health engagement will together control costs and pivot the sick-care system to one focused on well-being.

Deloitte points to three “future realities” in their modeling:

- A $3.5 trillion “well-being dividend,” those cost-savings generated by the shift toward prevention and early disease detection and the adoption of (appropriate, cost-effective) technologies

- Shifting spending toward well-being and social determinants of health earlier in health citizens’ life cycles

- A new health economy bringing about the “end of the general hospital as we know it,” a dramatic change in health care financing in the U.S., and a slowing of mass/general pharma manufacturing.

The second chart shows six developments that drive the future state of health care and spending in the U.S., including data sharing enabling better care coordination; interoperability resulting in price transparency and smarter spending on what works; equitable access shifting care to lower-cost, accessible settings away from capital-intensive inpatient care; empowered well-being, putting work-flows into patient-consumer-citizen hands as people “take ownership of health;” behavior change which is driven by behavioral economics; and, scientific breakthroughs focused on health-economic outcomes research and personalization.

Health Populi’s Hot Points: Deloitte is expecting “seismic shifts” over the next twenty years as the U.S. health economy moves from sick care to a system focused on well-being.

Health Populi’s Hot Points: Deloitte is expecting “seismic shifts” over the next twenty years as the U.S. health economy moves from sick care to a system focused on well-being.

There are three known unknowns in this scenario —

- Will consumers want to and adjust to greater self-care workflows, to take greater ownership of their own health and health care?

- How will privacy laws adjust to the massive flows of data from innumerable sources beyond the traditional health claim which won’t look or act like it does today. Personal health information will go beyond the medical, to include data flows generated by wearable technology, sensors on skin, implantables, digital therapeutics, home Internet of things-things, and stuff we cannot imagine 20 years hence.

- How will America’s 6,000+ hospitals adapt?

Let’s tackle tackle #3, as #1 and #2 are perennially covered here in Health Populi.

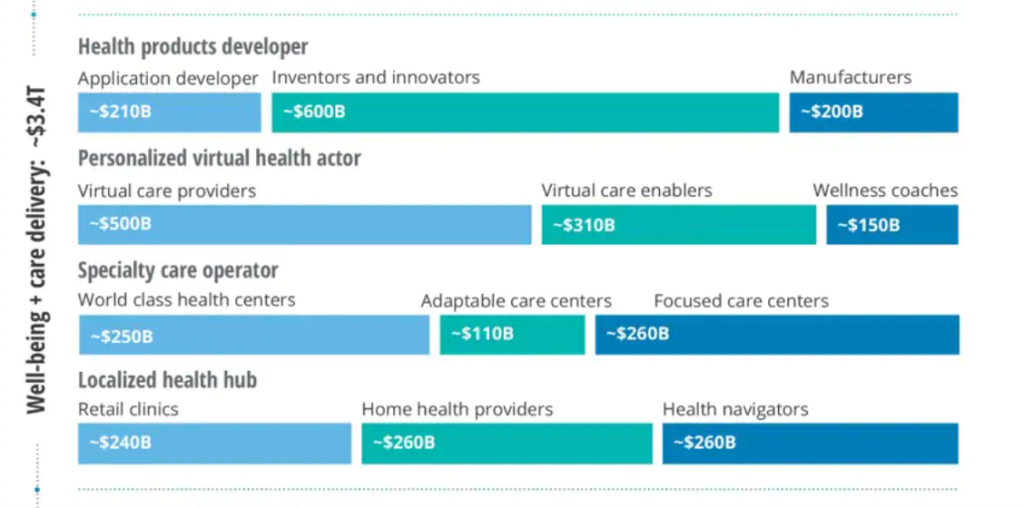

The biggest shift in this scenario is that $4 in $10 would be allocated to well-being and care delivery, and $3 in $10 for data + platform that informs cost-effective care.

This last chart comes out of Deloitte’s projections for three key components in the U.S. health care system for 2040, focusing on just the well-being + care delivery segment (the other two are the data + platforms, and care enablement segments).

This component breaks down into four categories of work flows and spending by personae or “new business archetypes”/actosr:

- Health products developers, with most spending going to inventors and innovators followed by application developers and manufacturers

- Personalized virtual health actors including virtual care providers, enablers, and wellness coaches

- Specialty care operators, featuring focused care centers, world class health centers, and adaptable care centers, and

- Localized health hubs such as retail clinics, home health providers, and health navigators.

There’s nary a “hospital” to see in this scenario. There are those care centers which are specialized and “world class,” and local health hubs.

The COVID-19 pandemic revealed many weaknesses in U.S. health care as it is currently organized, financed, and delivered. Health inequities and disparities, volume-based payment, and inaccessible, unhygienic physical plants were some of the areas the public health crisis highlighted for us to learn and grow from in re-imagining and re-building a more equitable, cost-effective, and safer health care system in America.

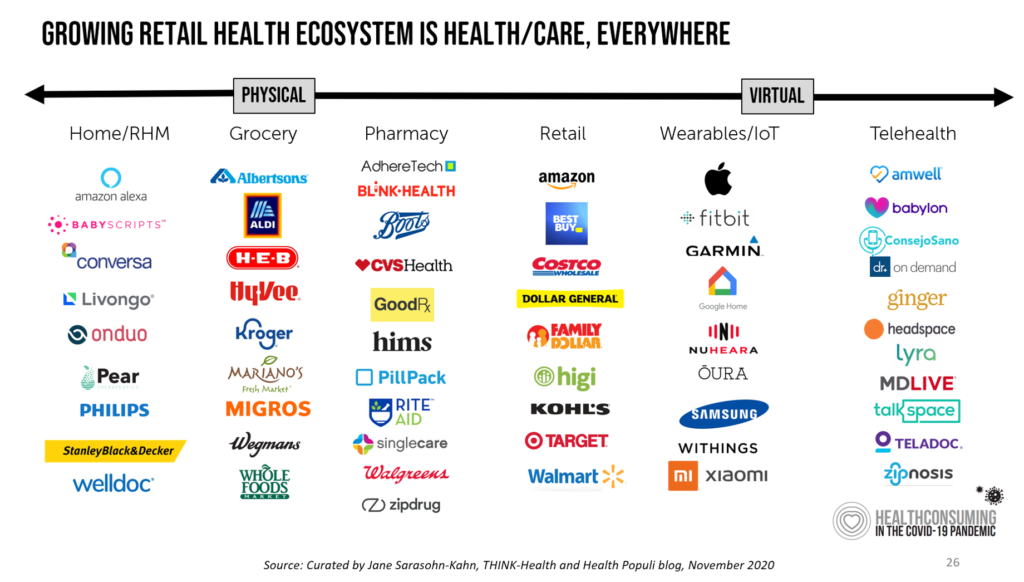

The value of care delivered at home and closer-to-home is part of this awareness, which is represented by the re-envisioned care delivery modes in Deloitte’s vision here. Deloitte provides a provocative argument for how to bend America’s unsustainable health care cost curve while enabling patients – morphing from consumers to health citizens “owning their care and health,” in Deloitte’s words.

The value of care delivered at home and closer-to-home is part of this awareness, which is represented by the re-envisioned care delivery modes in Deloitte’s vision here. Deloitte provides a provocative argument for how to bend America’s unsustainable health care cost curve while enabling patients – morphing from consumers to health citizens “owning their care and health,” in Deloitte’s words.

I share that vision with Deloitte, explained in my book, Health Citizenship — where we envision people “owning and not renting” their health and health care.

The past few years have birthed a growing roster of organizations serving up new models for primary care: the list includes CVS/health, Walgreens coupled with VillageMD, Walmart and its evolving approach to community-based primary care, and many new models for primary care targeting specific populations (from working age employed people to older folks in Medicare Advantage plans providing food and social determinants-focused services), among others.

U.S. hospitals have taken a huge hit in the COVID-19 pandemic, both financially and in terms of human capital front-line clinicians. Their ability to recover in 2021 and 2022 as the national economy heals and again grows will be a crucial time period to strategic plan and executive for a future that is not defined by a traditional inpatient bed.

For the past 15 years,

For the past 15 years,