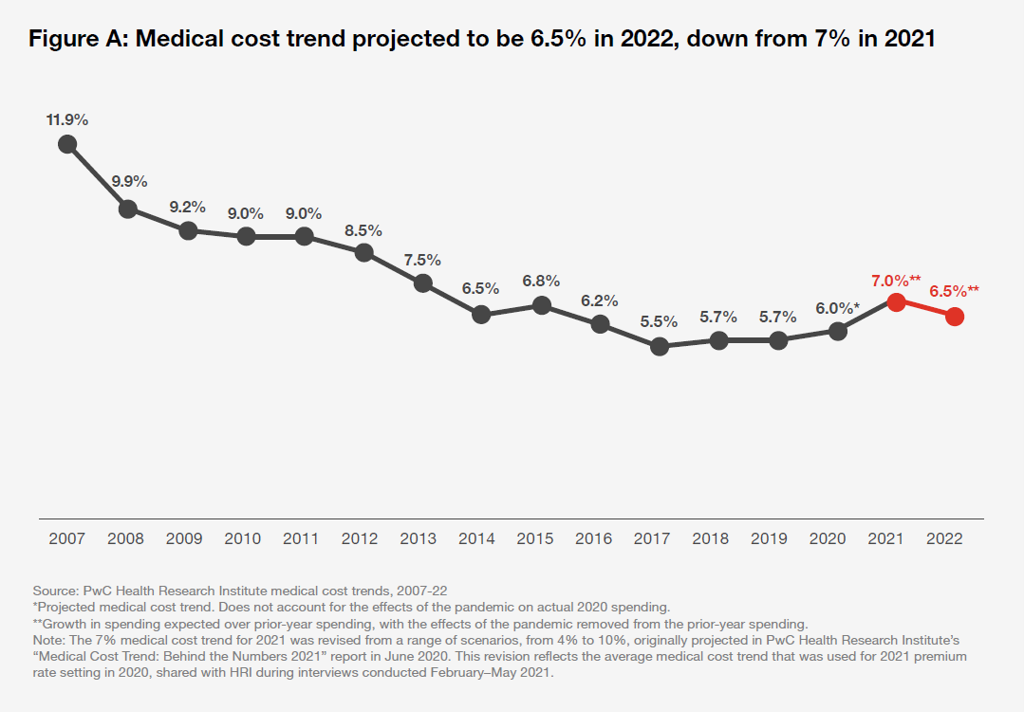

In the COVID-19 pandemic, health care spending in the U.S. increased by a relatively low 6.0% in 2020. This year, medical cost trend will rise by 7.0%, expected to decline a bit in 2022 according to the annual study from PwC Health Research Institute, Medical Cost Trend: Behind the Numbers 2022.

What’s “behind these numbers” are factors that will increase medical spending (the “inflators” in PwC speak) and the “deflators” that lower costs.

What’s “behind these numbers” are factors that will increase medical spending (the “inflators” in PwC speak) and the “deflators” that lower costs.

Looking around the future corner, the inflators are expected to be:

- A COVID-19 “hangover,” leading to increased health care services utilization

- Preparations for the next pandemic, and

- Growing digital health investments that will push patient utilization up.

The deflating, lowering-cost factors will be:

- Consumers looking to lower-cost sites of care and

- Health systems finding ways to provide more care using less resources.

What enables those deflating cost-reducers is the growing adoption of digital health tools, from telehealth and virtual care to self-care in patients’ hands at home and on-the-go via mobile health apps.

All those digital tools generate data, which must flow into some version of a patient health record to ensure the data are collected, safely stored, and accessible for diagnosis and sound action-making and -taking.

All those digital tools generate data, which must flow into some version of a patient health record to ensure the data are collected, safely stored, and accessible for diagnosis and sound action-making and -taking.

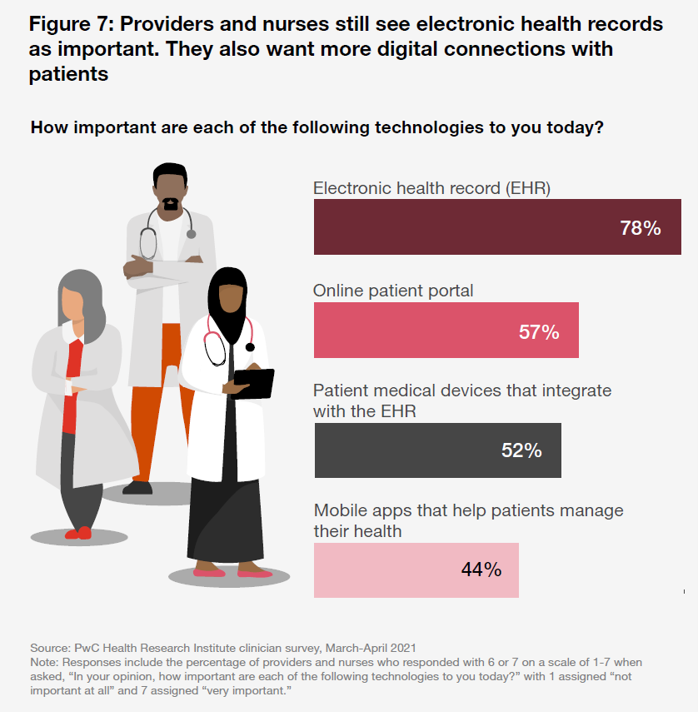

What a difference a decade makes for clinicians’ embrace of electronic health records. In 2021, 4 in 5 providers and nurses see EHRs as important, and increasingly demand digital interactions with patients.

These include the use of online patient portals (for 57% of clinicians) along with digital devices and mobile apps that integrate with the EHR as well as health patients manage their health in self-care mode, shown in the bar chart labeled Figure 7.

The pandemic accelerated many providers’ initial adoption of virtual care, along with their growing appreciation for the value delivered by digital health tools in patients’ hands and homes.

With that in mind, PwC found that providers plan to increase digital health investments (which is a cost-increasing factor in and of itself) across a landscape of tools focused on improving relationships with consumers and supporting health outcomes. These include remote monitoring tools for virtual check-ins addressing chronic conditions, more home-based care, emails and texts that nudge patients over time, digital pricing tools to support shopping for medical services, and better-designed portals that serve up more welcoming digital front doors.

Complementing that supply side, it’s important to note that most patients who have employer-based health insurance were willing to use digital tools to engage in their health care, such as chatting online with a health system’s website (say, via chatbot) or using a doctor’s or health system’s mobile app, based on PwC’s consumer survey from April 2020.

In September 2020, PwC surveyed consumers with employer-sponsored health insurance about their preferred locations to receive a COVID-19 vaccine within one year of its approval. Consumers expressed different vaccine site preferences depending on their ethnicity/race and age group. Sites included:

In September 2020, PwC surveyed consumers with employer-sponsored health insurance about their preferred locations to receive a COVID-19 vaccine within one year of its approval. Consumers expressed different vaccine site preferences depending on their ethnicity/race and age group. Sites included:

- “My” doctor’s office, favored by more people who were White or Asian, and those 45 years or older

- Retail clinics or pharmacies, more preferable to Black Americans and slightly more younger people, and

- Urgent care clinics or freestanding ERs, preferred by more Latinx patients.

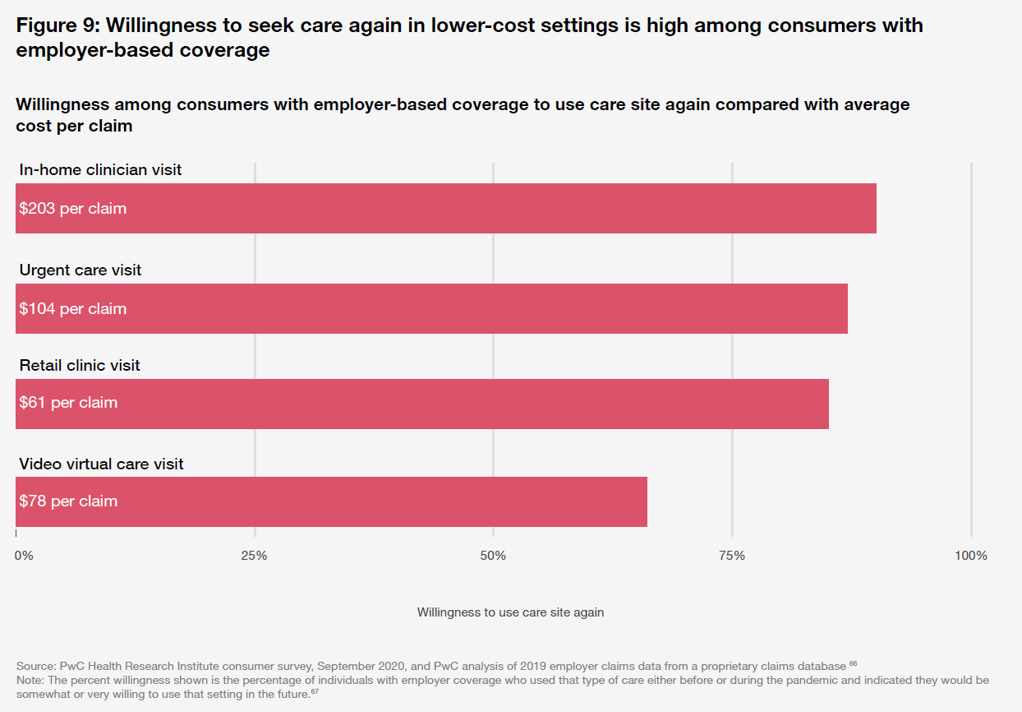

This relates to another key data point that illustrates patients’ shift to a health consumer mindset: their willingness to seek care in lower-cost settings based on costs.

The chart labeled Figure 9 shows consumers’ different levels of “willingness” to seek care in each of four locations based on their employer-based health care coverage. The person’s level of willingness varies depending on the average cost per claim for that site.

For example, over 70% of patients are willingness to use a video virtual care visit based on the claim cost of $78. For retail clinics costing $61 per claim, 4 in 5 people would be willing to get care there. At $104 per claim, nearly 9 in 10 consumers would be willing to visit urgent care, and for a clinician’s visit to the home, Marcus Welby-style, close to all patients would be willing to receive a “house call” from a clinician based on a $203 cost per claim.

It is also notable that consumer-patients dealing with complex chronic conditions were more interested in using telehealth, based on PwC’s consumer survey. One-half of people with employer-sponsored health insurance managing complex chronic disease used telehealth as of September 2020, and 95% of them would consider using it again.

Health Populi’s Hot Points: The COVID-19 hangover will be a key inflator of medical costs in 2022. This will be driven by care postponed and returning as non-urgent “in the same form” as would have been expected during the pandemic; and, care postponed and returning with greater acuity requiring more intense attention and resources. The latter is higher-cost care than would have been expended in real-time had the pandemic not kept patients away from doctor’s offices and hospitals.

Consider in the postponed/higher-acuity patients: a cancer diagnosis/prognosis that advanced from Stage 1 to Stage 3, or prediabetes that grew to full-blown Type 2 Diabetes.

Furthermore, there is another COVID-19 “hangover” that’s a real epidemic within and post-pandemic: growing mental and behavioral health prevalence, which we increasingly acknowledge as a next-normal for U.S. population health burden.

Furthermore, there is another COVID-19 “hangover” that’s a real epidemic within and post-pandemic: growing mental and behavioral health prevalence, which we increasingly acknowledge as a next-normal for U.S. population health burden.

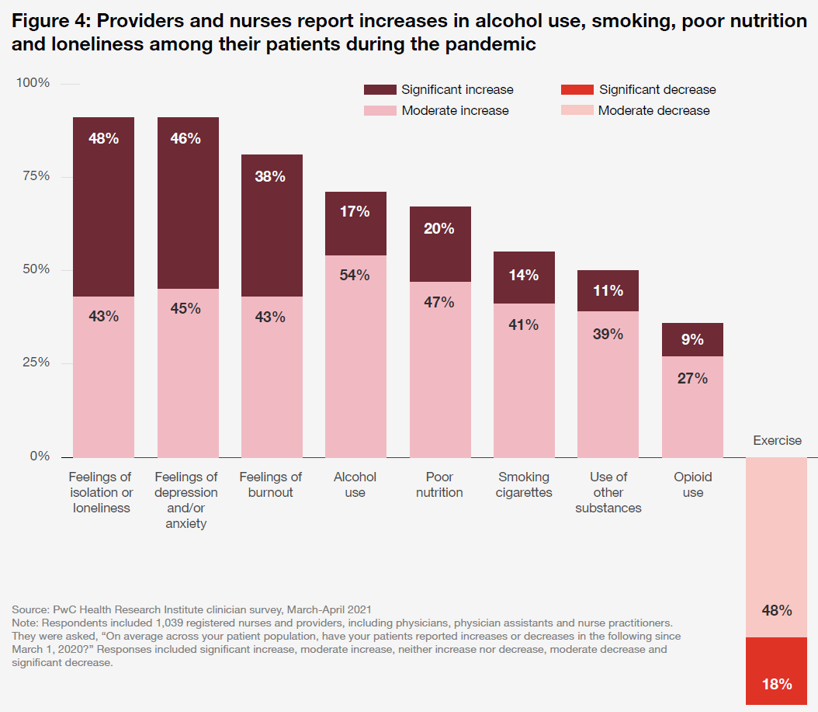

This last chart (Figure 4) gauges behavioral health issues for patients during the pandemic, from PwC’s clinician poll of March-April 2021.

Note significant increases in feelings of isolation and loneliness and depression and/or anxiety for about 1 in 2 patients, and moderate increases for the other half of consumers.

Feelings of burnout were significant for one-third of patients, with another 43% feeling a moderate increase in burnout.

Alcohol use among consumers grew moderately for 54% of people, with another 17% confessing to a significant increase — net, that’s 71% of consumers using alcohol more during the pandemic. [This discussion on “supersizing” of alcohol purchases via ecommerce tells part of the story on growing alcohol use in the U.S. during the public health crisis. The Atlantic offered this take this week].

Other behavioral health issues that bode poorly for consumers’ physical health are the 67% of consumers engaging in poor nutrition habits during the pandemic, 50% of people using substances (not opioids), 55% smoking with 14% admitting to significantly increase tobacco use, and 36% increasing use of opioids. Note on the “decrease” half of the graph is exercise, with 18% of people significantly reducing their physical activity, and one-half of Americans moderately decreasing exercise.

As we ponder health care utilization and medical spending in 2022, the wild cards that could increase PwC’s 6.5% forecast of medical trend will be (1) just how quickly consumers can/will change their lifestyle behaviors (which contribute to the noncommunicable diseases of the heart, diabetes, respiratory conditions, and many cancers) and their return to preventive care and health screens to catch cancers and other conditions earlier rather than later.